I have sent out a couple of emails about investing strategies through my mailing list lately and it has generated some interesting discussion about certain stocks. Two of them were brought to my attention as they are somewhat similar: IGM Financials (Investors Group) and Power Corporation. Since I have covered IGM in my best 2012 dividend stocks and picked Power Corporation for 2013 (download the book here), I thought of sharing more views about both stocks. Here’s my IGM stock analysis.

IGM Financial (IGM) Business Description:

IGM Financials is mostly known for the name Investors Group, the largest mutual fund company in Canada. The company also manages Mackenzie Investments and belongs partly (57%) to Power Corporation (POW). Investors Group provides financial planning services along with mutual funds and insurance services. Through a partnership with National Bank, they also provide regular banking products and loans to their clients.

Investors Group has been particularly strong in Western Canada. This was a happy coincidence for them as the oil industry has propelled Alberta to become the richest Canadian province. IGM has also been known for their aggressive leveraging strategy (borrowing to invest). During the 2000s (before 2008), this strategy gained a lot of adept investors and you can bet that most consultants made a lot of money out of this “new” way of getting funds from their clients.

Their latest quarter results (were published on Feb 8th) were on target with analysts’ expectations. Unfortunately, they have failed to increase their sales in 2012 compared to 2011 (5.78 billion Vs 6.02 in 2011). I guess that their high MERs funds have started to hit their salesforce.

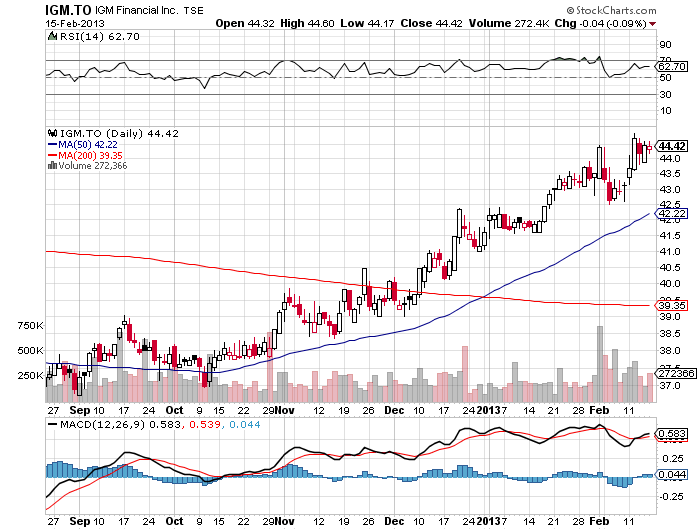

IGM Stock Graph

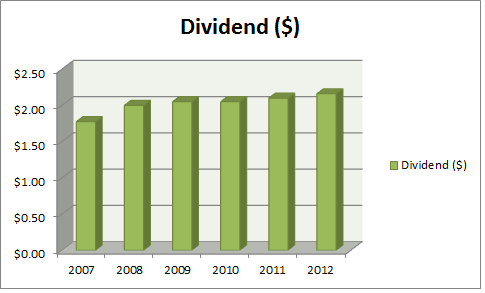

IGM Dividend Growth Graph

As you can see, there is a very small dividend growth over the years but nothing too impressive. The current payout ratio (65%) leads me to think that we won’t see a huge dividend increase in the upcoming years. The dividend yield is relatively strong for a financial company (over 4%) which makes it an interesting stock nonetheless.

The Company Ratios and Financial Info:

Ticker IGM CN Equity

Name IGM Financial Inc

Dividend Metrics

Current Dividend Yield 4.94

5 year Dividend Growth 3.91

1 year Dividend Growth 2.38

Company Metrics

Sales Growth (1 year) #VALUE!

Sales Growth (5 year) -3.24

EPS growth (5 year) 11.8

P/E ratio 14.66

P/E Next Year 13.06

Margins growth #VALUE!

Payout ratio 64.56

Return on Equity 18.43

Debt to Capital Ratio 0.14

The company shows a high ROE and Earning per shares growth for the past 5 years. The fact that IGM had it rough in 2012 makes it a good contender to bounce back in 2013. Still, I don’t expect impressive sales from IGM this year.

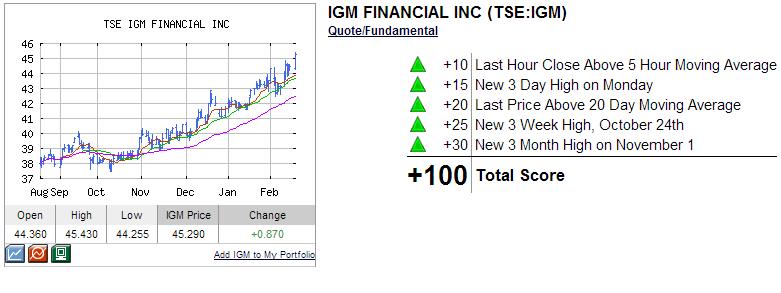

IGM Stock Technical Analysis

IGM is currently trading on a strong uptrend. It might be a good time to acquire this stock. Click here to get a free stock analysis report on IGM.

IGM Financial Upcoming opportunities and dangers:

IGM is the Canadian leader in mutual funds sales with over $120 billion in total assets under management. They are still showing a very strong position and I would not underestimate their salesforce (which is their strongest asset in my opinion). They have successfully built a fence around their clients by offering all banking products through the National Bank back office (coupled with a non-competing clause). During volatile markets, sound financial advice is needed by investors and IGM will be there to meet clients’ requests. They show a positive 5 years sales growth despite a disastrous year in 2008.

With the coming of low fee investments such as Vanguards’ products, high MER funds such as IG’s and Mackenzie will face fierce competition. Their added value through sound financial planning will be challenged by clients who will require additional reasons to pay over 2% in management fees. New legislation around leveraged loans (a popular strategy at IG) may also affect mutual funds sales.

Final Thoughts on IGM Financial

If you are looking for a good financial stock paying a healthy dividend IGM may be a good pick for a few years. However, when I look at the long term perspective, I really wonder how IGM financials can continue to sell such high MERs fund competing with Vanguard for example.

I think they will have to review their business model and a good financial planner won’t be good enough to keep clients paying over 2.00% in management fees. What do you think?

Disclaimer: I do not hold any shares of IGM

I agree regarding the fees. They not only push high MER funds but they have “Portfolio Funds” that are basically funds containing 4-5 of their other funds. The Portfolio fund has a 2% MER while the constituent funds have the regular high MER’s of >2%. Imagine charging 2% to bundle 4-5 funds?? Fees on fees, what a great concept!! How exploitive.

@Dale,

How exploitive, but how profitable 😉 hahaha!

the IG model of “wrap products” is the biggest concern for myself. I understand paying a fee. I would gladly pay a hefty fee if it allows me to mitigate risk and give me additional performance. The problem is that this is not happening. the recent MER reductions that they made last year are a good indication that they know this too.

For all it’s worth, a lot of my relatives out west are dropping Investors in favor of ETF’s. I own PWF for the dividend and some growth (more diversified).

Good analysis. Personally, I prefer to own the parent company (PWF or POW for that matter) and limit my exposure to just IGM. With PWF you get exposure to GWF as well which is good diversification. I assume you’ll get to that with POW. The ownership structure of those corporations is definitely most interesting.

Cheers!

@Passive Income Earner / Michel

you will like today’s analysis as I’ve come to the same conclusion 🙂

I would not own shares of IGM because they are experiencing severe net redemptions as customers flee their high fees. They are making money now but look at what is happening to AGF. If you can’t see future growth in a company, you should not be investing. I would not own POW for the same reason. GWL is a good company though and I would consider them.