If you live in Canada, you probably heard about ScotiaBank’s catchy line you are richer than you think. They imply that they can improve your financial situation so you can have a stronger balance sheet. If I was a competitor, I would come up with the opposite line: You Are Poorer Than You Think. If you think of all the fees and transaction costs you pay to have your portfolio managed by someone else, you are truly poorer than you think.

I totally understand that not everybody could be or wants to be a DIY investor. As a matter of fact, I think that financial advisors and brokers (I mean the honest ones amongst this group, hahaha!) have a real utility for most investors. They will provide solid financial advice, will take care of retirement planning for you and will also manage your funds. These services obviously have to be charged, nothing is free. However, have you ever took a second to consider how much you pay in fees and transaction costs and how it will affect your portfolio in 10, 20, 30 years? Yeah I know, it takes too long to build the excel chart, right? Let me do it for you!

One Situation – Four Scenarios

I’ll start with a totally fake situation that could be pretty much related to anybody:

A young investor at the age of 30.

Investing $5,000 per year on January 1st.

He plans on retiring at the age of 60 (so 30 years worth of savings).

At the age of 60, he wants to withdraw money for the next 20 years (so until he is 80).

Average investment return before fees at 5%.

I’m not considering the rate of inflation since I’m not doing a retirement plan, I just want to highlight the difference of management fees and transactions costs in one’s account over the next 30 years.

Scenario #1 & 2 Investing in Mutual Funds

The classic response for most young investors is to start with mutual funds. This is not a bad idea, especially if you don’t know much about the stock market. It will give you a better picture of how it works and how money is managed. For scenario #1 and #2, I’ve taken the hypothesis of an investor using mutual funds to grow his nest egg.

In scenario #1, our young fellow is taking the first mutual fund available and invests with a management fee of 2%. In scenario #2, the investor manages to find a cheaper mutual fund at 1% MER.

Scenario #3 & 4 DIY Investor with an Online Broker

For the other two scenarios, I’m considering that our investor likes to read about the stock market and prefers to invest by himself. Scenario #3 shows the results if he picks the first online broker he sees and pays $15 per transaction. Assuming he makes 10 transactions (buys or sells) per year, this total to $150 in transaction fees. In scenario #4, our young investor does his research and finds a quality online broker at $4.95 per trade. He does the same 10 transactions to either buy more stocks or to manage his asset allocation.

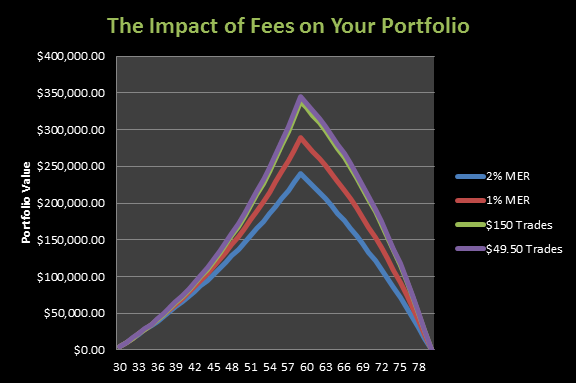

The Results in 1 Graph

You can probably tell by now that scenario #1 and #2 will affect our investor’s retirement plan greatly since the fees grow according to the value of the portfolio. But the graph will definitely show you how a 1% MER fund represents so much money over 30 years of savings and 20 years of retirement.

The Shocker in 1 Chart

The chart shows clearly that investing with MERs as a percentage of your assets is a killer. The following chart will show you that even if you pick an online broker, even the small difference of paying $4.95 per trade instead of $15 makes a huge difference. We are talking about $12,000 more in your pocket over the long haul. I don’t know about you, but $12,000 is a lot of money!

Scenario Investment Value Peak Total Fees Paid Amt Available at Retirement Total Withdrawals

2% MER $240 848.41 $120 287.57 $15 000.00 $300 000.00

1% MER $289 078.69 $70 373.30 $19 700.00 $394 000.00

$150 Trades $338 838.12 $7 650.00 $25 000.00 $500 000.00

$49.50 Trades $345 515.23 $2 524.50 $25 600.00 $512 000.00

In Which Scenario Are You?

The real question is how much you truly pay to invest in the stock market. Now you know that paying more fees than you should has a dramatic impact on your retirement. We are talking about a difference of $212,000 between the worst and the best scenario! Fortunately, there are great online brokers offering low cost transaction fees.

From the top 8 online brokers, I consider that TradeKing is the best for cheap transactions and best customer service:

The fees are one of the reasons that I hate mutual funds. Outside of my 401K, I invest in individual stocks and just pay the small brokerage fee.

And recently (in canada at least) if you invest with some of the online brokers you can buy and trade ETFS with no fees 🙂

I always like your blog Mike. DOn’t always agree but even then I could still learn of some angle I had not thought of. One of the things I like is that you are down to earth – you still believe $12K is a lot of money. Some people have lost track of what it is to “work” for money and think it will fallout of the sky. Only thing I have seen fall from the sky is snow and rain with an occasional meteorite. Unless you are on a golf course in a rain storm and get your rear end tickled LOL

You may save fees by doing your own trading, but do you save money if you make bad trades? For someone who is willing and has time to do their own homework, I agree you can certainly save money. But there is more to saving for retirement than throwing darts. There is estate planning, distribution considerations, tax planning, and so on…

Just as you can be your own lawyer, sometimes you are better off paying for some help.

Hello Roger,

I totally agree with you. Trading on your own is not always the best solution. However, even if you pay someone, you could certainly appreciate how a 0.50% in fees would make a difference on your porttfolio over the next 40 years.

thx for commenting!

Mike.

I understand this concept, I am just wondering if using an advisor with higher fees may still be beneficial as they may be able to get a higher return on your investments than you can doing it yourself

Hello Patricia,

the thing is the advisor doesn’t do much; it’s the mutual fund that comes with higher fees. If you select a high-end broker that has an amazing track record, it can worth it. It all depends on your financial background and your ability to manage a portfolio on your own.