Following my analysis on Mattel (MAT) and Hasbro (HAS) from last week, I’m closing this toy stock series with the most famous company in the eyes of children: The Walt Disney Company (DIS).

Note: The stock is currently showing a dividend yield of 1.14%. This definitely does not fit my Dividend Growth Investing Model. But the company has recently started to increase its dividend and it makes a great comparison to Mattel and Hasbro who are pretty much alone in the toy industry paying distributions over 3%.

Disney (DIS) Business Description:

If you have been hiding under a rock for the past 80 years, you may ignore that Disney is THE reference for family entertainment. The company is divided into four sectors:

#1 Media Networks (ABC Family, ESPN, Disney Junior, etc)

#2 Parks & Resorts (you need to visit one in your life)

#3 Studio Entertainments (Pixar, Walt Disney Pictures, Marvel banners)

#4 Consumer Products (Mickey Mouse, Cars, Disney Princess, Winnie the Pooh, Toy Story, etc, etc, etc)

Founded in 1923 by Walt & Roy Disney as The Disney Brothers Cartoon Studio, Disney is today the world’s largest media conglomerate in terms of revenues. Disney has recently hit several home runs with the acquisition of Marvel where they pump a Heroes movie out every six months. After the huge box office success Avengers in 2012, Disney is coming back this year with Iron Man 3 and Thor – The Dark World. This is not to mention their animation studios produced Brave, Frankenweenie & Wreck-it-Ralph (which I really liked!) all in the same year.

The ability to generate important movie success is amplified tenfold by their talent to produce fifty-six-billion of connected consumer products. As it wasn’t enough, Disney bought the license to “close” the Star Wars story with the “last” trilogy.

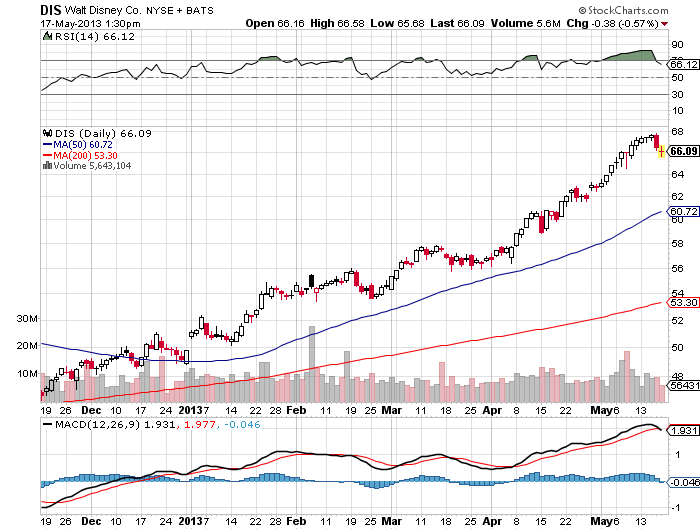

DIS Stock Graph

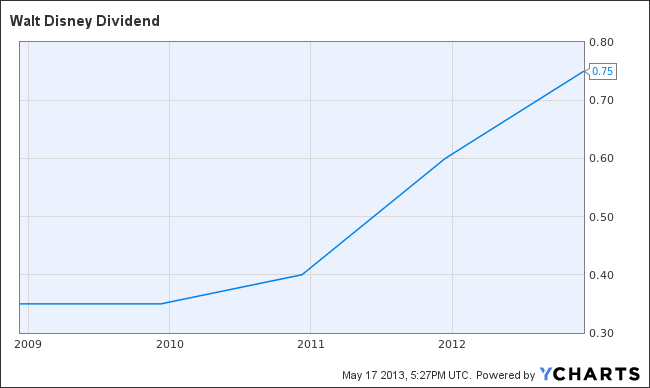

DIS Dividend Growth Graph

As I mentioned at the beginning of my analysis, DIS is not known as a super powered dividend stock. With a small yield of 1.14%, it could never be part of my portfolio. However, the recent dividend payout growth is interesting if management keeps it this way. The dividend growth over the past 5 years is at 16.47% while they made a big jump last year as per the following graph:

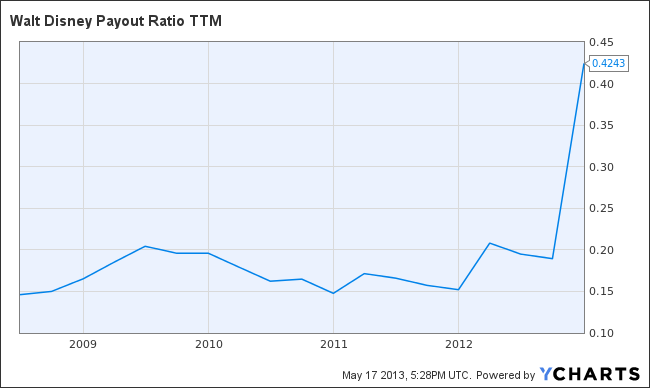

Most importantly, Disney shows they have huge room to increase their payout in their future with a current payout ratio under the bar of 50%.

But don’t get me wrong, with their massive projects, Disney requires a lot of liquidity to fund them and apply their magical marketing recipe. If I had the choice, I think I would buy the Disney marketing recipe over Coca-Cola’s magic formula ;-).

The Company Ratios and Financial Info:

Ticker DIS US Equity

Name Walt Disney Co/The

Dividend Metrics

Current Dividend Yield 1.16

5 year Dividend Growth 16.47

1 year Dividend Growth 25

Company Metrics

Sales Growth (1 year) 3.39

Sales Growth (5 year) 1.83

EPS growth (5 year) 6.91

P/E ratio 20.92

P/E Next Year 16.53

Margins growth 1.74

Payout ratio 18.94

Return on Equity 14.31

Debt to Capital Ratio 0.15

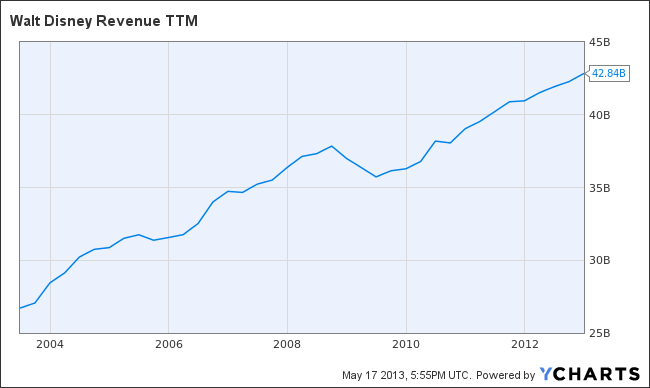

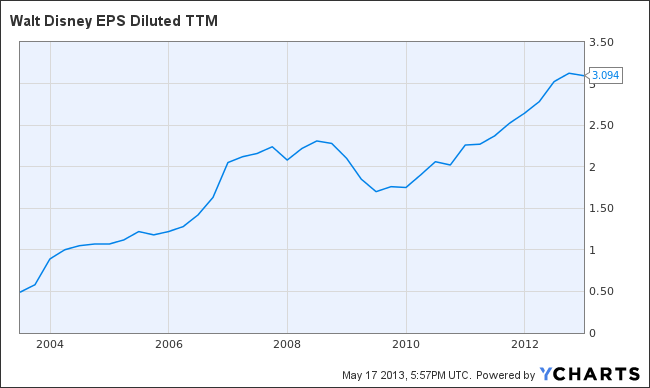

When I look at the numbers, I can’t be disappointed. Both sales AND profits are up while the company boosts its dividend. You can even go back ten years and still see an awesome growth in revenues:

Same story with the earnings:

We can see that after the economic crisis of 2008, they rapidly recuperated their swing to boost 2011, 2012 and now 2013 sales and profits. The company is definitely solid.

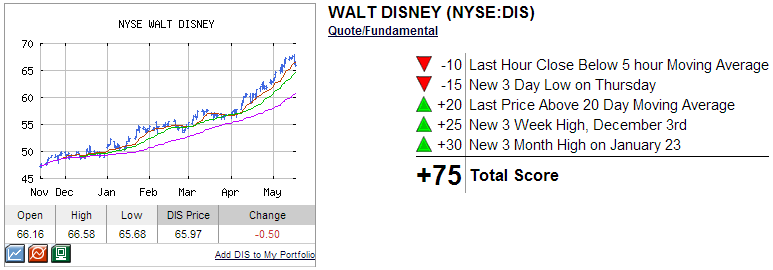

DIS Stock Technical Analysis

DIS is currently trading on a strong uptrend. It might be a good time to acquire this stock. Click here to get a free stock analysis report on DIS.

Disney Upcoming opportunities and dangers:

With such a large brand portfolio coupled with multiple acquisitions, Disney counts on several opportunities to continue to grow. Since Americans have cleared a part of their debts during the past three years, chances are they are more inclined to spend more in the upcoming years in entertainment.

The other point that convinced me about the company was my personal trip to Disney World last winter with my three kids. Everything was perfect. I mean EVERYTHING. Their ability to think about the unthinkable and make the customer experience his best family vacation souvenir ever is almost unreal. A company with such dedication to detail is definitely a keeper for a portfolio.

As for the dangers, we often mention their media network division to be at risk seeing possible cable erosion. This could be a possibility if Disney’s brand wasn’t as strong in our minds. Kids will want to see Disney’s cartoon and movies while adults will always be looking forward live sports on TV through ESPN.

The downside? A relatively high P/E ratio currently sitting at 20. Considering the company’s growth potential in the upcoming years (do I have to mention how much money you make on a Star Wars Episode?), this is a calculated risk. Mind you, several great stocks are trading around 20 P/E ratio right now. It might not be the best time to buy the stock, but I don’t think there will be a major pull back either.

Final Thoughts on Disney

The more I read about Disney, the more I’m seduced by this company. It bites me that it doesn’t pay a higher dividend… But I’m still considering this stock as it has been paying a dividend for the past 14 years. Based on my analysis, DIS looks like a great complement to my portfolio. Still, I’m not making any trades at the moment.

Disclaimer: I do not hold shares of MAT, HAS or DIS

I’ve held DIS since Aug 2004. I’ve collected $1,754 in dividends since then. In many ways I wish I’d only bought DIS instead of focusing on what I calculated at the time to be the better companies KO and GE. Learned at lot since then. I’ll continue to hold my KO and continue reduce my GE and add to my DIS

Yeap, with this yield DIS will not be in my portfolio either. But we are going to visit Disneyland next month, when the kids will be out of school. I am excited too!

Great write up. DIS is definitely a tough one for dividend investors. I tend to dismiss a stock that yields under 2% as a non dividend stock. As you point out though there is more to investing that yield when you are in it for the long term and total return after dividend growth. Lots of positives for the future.

I don’t have MAT or HAS but I did buy some DIS earlier this year. I think it’s great diversified and innovative company 😀 I was anticipating that Iron Man 3 would be very successful in theaters and the long term value would come from other Marvel, and Star Wars films. I like how Disney acquires and then integrates other companies into itself. When Disney wanted to hire the most talented computer graphics engineers in the world, instead of contacting those individuals it just bought Pixar, lol. Then it leveraged Pixar’s renowned resources, talents and technologies to help improve its own already established Walt Disney Animation Studios. Pixar gets massive funding on its projects like Toy Story 3, and Disney gets expertise to experiment with its own originals like Wreck it Ralph. Awesome synergy 😀 The current p/e is a little high, but when Warren Buffett paid more than he initially wanted to for Heinz he said said it’s okay to overpay a little as long as you’re paying for a good business 😀

I have thought about buying Disney, but the high valuation has stopped me so far. The company does own a lot of strong brands however. My only concern is that the movie is generally very cyclical – you can never say if you are going to have a blockbuster or not – altough the DIS franchises have some awesome movies that will probably keep making $$ for years to come.

I’ve held on for a while, believing that ESPN was really a genius business model but, as a sports fan I am getting increasingly tired of their reporting and antics. There are places online that do a better job of reporting, being thorough or just giving me what I want quickly and efficiently.

That said, they do hold some lucrative contracts to exclusively broadcast college football games which is big money and increases its interest year-after-year.

In a recent post in my blog, I looked into what movie would come next from the Star Wars franchise, illustrating that the number of different generations of fans Disney will be targeting, will allow the renewed franchise to easily break all box office records. Let’s not forget the ridiculous amount of swag produced: clothing, toys, games, etc.