For the past decade and a little bit longer, Canadian Banks have been a model of stable growth and security for investors. Their profits grow at the same rhythm as their dividend growth and they never jeopardized their financial health for the sake of investors’ greed. They were accused of being boring and conservative for several years until the market crashed in 2008. At that time, Canadians banks rose in the rankings to the top of the world’s safest banks as they found the perfect balance between security and profitability. If banks are the heart of an economy, it appears that Canada has the most solid blood pumping machine on the planet.

Canadian Banks Were the Place to Be – Is it Still the Case?

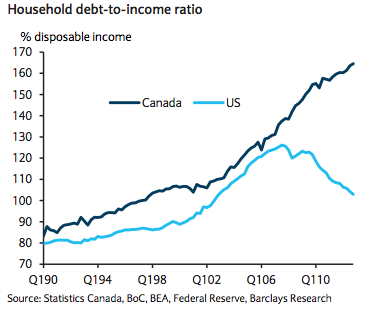

I’ve expressed my concerns about Canadian Banks a few times this year and haven’t changed my mind during my most recent asset allocation update. A simple look at the household debt-to-income ratio should convince you of my opinion:

As you can see, while the US debt ratio dropped during the crisis and was brought back close to 100%, the Canadian debt ratio has continued climbing higher and higher. Variable interest rates are not going up in 2013 but fixed mortgage rates started to climb. We saw several Canadian banks hitting their margin on those rates in order to attract new clients. The Canadian housing market is slowing down and banks can only steal customers from each other in order to grow their market share. This means they will continue to hurt their margin for the sake of acquiring new clients. A mature industry in a mature market; I don’t think there is much growth to be seen in the short term. You can see how Canadian banks have performed so far compared to the Canadian Index (everything is pretty is in slow motion right now!)

Different Country, Different Story

In the US, financials were hit dramatically in 2008 as they played too much with toxic assets. These days finally seem to be over as banks have cleaned their balance sheets, took their losses, with some Gov’t help (read cash) and they seem to be back on the profitability track! A quick look at some major players, JP Morgan (JPM), Wells Fargo (WFC), Citigroup (C ), Bank of America (BAC), show you how they perform compared to the overall market:

Over the past few weeks, Wells Fargo declared a climbing profit of +20%, Citigroup did even better with +41% (financial analysts expected +17%). JP Morgan showed EPS of $1.60 compared to $1.21 last year.

These great results are a combination of two factors:

#1 Banks have cleaned up their balance sheets and they are now dealing with a healthy credit portfolio

#2 The US economy keeps going up at a steady rate. We would all hope for a bigger growth but the economy is strengthening quarter after quarter.

The US housing market is doing a lot better and this should help banks to grow their credit portfolio.

Which Financial is the Best Dividend Pick?

From the four stocks mentioned above, I would put my $2 on Wells Fargo. Both JPM and WFC show a dividend yield slightly under 3% and the other two are far from being dividend stocks right now with 0.29% (BAC) and 0.08 (C) dividend yield!

I’ve pushed my research a little further to see other financials paying interesting dividend yields. Most of them are not too generous with their payouts:

PNC Financial Services (PNC): 2.34%

US Bancorp (USB): 2.46%

Black Rock (BLK): 2.49%

At the beginning of the year, I selected Wells Fargo (WFC) as one of my top dividend stocks for 2013. This stock is currently up by 26.45% and has increased its quarterly dividend from $0.25 to $0.30 per share this year. Sales increase steadily while profit climbs up due to a better economic environment. I’m pretty confident Warren Buffett’s bank will continue to do well until the end of the year.

Final Thoughts on the Banking Industry

In light of my analysis, I would not drop the hammer on Canadian banks as they still show very strong metrics and high dividend yields (all of them are paying over 4% right now). This is definitely a good pick to build your core portfolio. On the other hand, I would not expect much growth from this industry for the next 12 months. We will have to wait until the housing market bubble deflates (or bursts!) to see profits climb as high as the good old days of the 2000s.

When I look at the US banking industry, I see companies that had a hard time going through the most recent recession but their main problems are finally over. I expect them to raise their dividend payout as their financial results get better. If you take a bet on a stock already paying between 2.50% and 3%, you may end-up with a solid profit and still rack-up a higher dividend in the meantime.

Readers; what do you think about Canadian and US banks? Where would you put your own $2?

Disclaimer: I hold shares of BNS and NA.

What percentage of the Canadian banks profit comes from mortgages? How is their bottom line affected by a drop in house prices?

As you pointed out, profits are looking pretty good for many of the banks. I’m a big fan of WFC and JPM.

Hello Bram,

the % of profit directly generated form the mortgage business is not that big. Most banks make roughly 30% of their profit from their retail business (which include mortgages). However, if they have to suffer default, mortgages write-off hurt a lot as this money doesn’t come back.

Most banks make over 30% of their profit from trading. A housing market slump would also affect this part of the business.

Big fan of WFC.

Might own JPM at some point.

Not buying C or BAC. Stay away.

I think I missed the boat on WFC. I was focused on the fact that revenues have not been growing since 2009, and that profit growth came only from a reduction in the provisions for loan losses.

Luckily, I don’t lose money from mistakes like these ones. 😉

What did you like about WFC, to make it into your best stocks for 2013 Mike? I am just curious.

Hey DGI,

I took aside the revenues growth for banks since 2008-2009 had been very hard for all banks. Therefore, simply going throught the restructuring process and cleaning their “bad loans” was a long and painful process.

Net income has been increasing since 2009 in a steady basis, the profit margin is going up slightly (which is pretty good for banks) and since 2010, dividend has been back on the growth side.

I think the worst is behind US financials and they now may be worth a closer look, what do you think?

Good article. I hold almost everything in Canadian banks and have for years. One thing to remember is that the percentage of revenue from outside of Canada is growing nicely as they strike out to be truly international brands. This is a bit of a hedge against Cdn market angst.