What are the best Canadian dividend stocks for 2025? Do you think the market will continue to rise, or will we finally hit the crash everybody is talking about?

I don’t really worry about where the market will go, to be honest. What really matters is how many dividends I will receive in the next 12 months. I can tell you it’s going to be more than last year. Although following the market is like watching a tennis ball bouncing up and down, focusing on dividend growth alleviates the stress.

It’s never easy to pick stocks in an overvalued market.

Here’s a shift of perception I’d like to suggest: look at the amount of dividends you receive each month or each quarter:

Keep your eyes on the prize: dividend growth!

Which Canadian Dividend Stocks Should be in your portfolio for 2025?

Today, I’m picking companies that will pay and increase their dividends and likely provide you with a nice capital appreciation. The selection methodology of those companies is explained in this article:

What should a Dividend Growth Investor buy in 2025?

Alimentation Couche-Tard (ATD.TO)

Business model

ATD is engaged in convenience and mobility, operating in about 29 countries and territories, with over 16,700 stores, of which almost 13,100 offer road transportation fuel. With its Couche-Tard and Circle K banners, the Company is an independent convenience store operator in the United States, and it is engaged in the convenience store industry and road transportation fuel retail in Canada, Scandinavia, the Baltics, and Ireland. It is also in Poland, Hong Kong Special Administrative Region of the People’s Republic of China, Belgium, Germany, Luxembourg, and the Netherlands. Its North American network consists of about 17 business units, including 14 in the United States covering 47 states and three in Canada covering all 10 provinces. It operates a broad retail network across Scandinavia, Ireland, Poland, and the Baltics through seven business units in Europe. Its operating brands include Circle K, Couche-Tard, and Ingo.

What was the story?

I won’t lie; 2024 was not great for Couche-Tard. This creates an opportunity we haven’t seen in a while.

Things are changing quickly around the 7-Eleven deal. ATD has tried to get to the negotiation table to acquire 7-Eleven for a few months now. The Japanese company is trying all means to stay Japanese. The latest chatter was that the son’s founder would buy it back and make it private. The market liked the idea, and the ATD share price rose again. This story isn’t over yet, one way or another.

For 2025, I see ATD striking another acquisition. After all, it’s in its DNA. If it’s not 7-Eleven, it will be another chain (maybe Casey’s?… it tried to acquire CASY in 2010). ATD must gain more expertise in organically growing by selling ready-to-eat and fresh produce. This is how they can mitigate the impact of slowing fuel and tobacco sales over the next 10-20 years.

Get 6 other ideas that should crush 2025 and beyond for a stress-free retirement

Each year, I compile a list of 20+ stocks expected to perform better than the market.

You can download 6 more companies of my top 27 for 2025 right here:

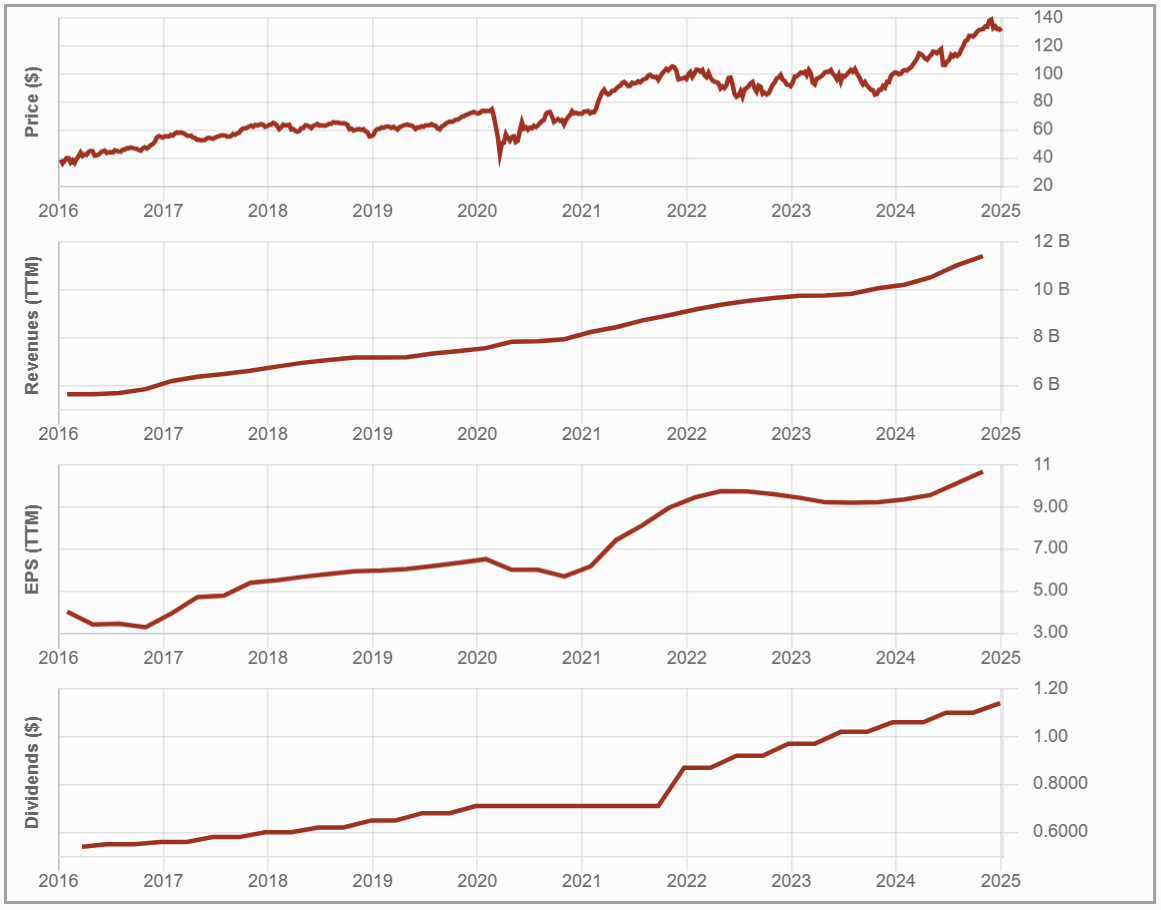

National Bank (NA.TO)

Business model

NA operates as an integrated financial group. The Bank operates through four segments: Personal and Commercial, Wealth Management, Financial Markets, and U.S. Specialty Finance and International (USSF&I). Its Personal and Commercial segments include banking, financing, and investing services offered to individuals, advisors, businesses, and insurance operations.

Its Wealth Management segment includes investment solutions, trust services, banking services, lending services, and other wealth management solutions offered through internal and third-party distribution networks. Its Financial Markets segment includes corporate banking, investment banking, and financial solutions for large and mid-size corporations, public sector organizations, and institutional investors. Its USSF&I segment consists of the specialty finance services provided by its subsidiaries, Credigy Ltd. and Advanced Bank of Asia Limited.

What was the story?

There is no secret here as I’m a National Bank fan. The bank seems to have done everything right over the past 15 years. This big transformation converted a small provincial bank into a serious player in capital markets and the private wealth industries. The Bank is expected to complete a key acquisition of Canadian Western Bank in 2025 which will bring more capital onto its balance sheet (supporting capital market lucrative operations), more synergies (high cross-selling opportunities between CWB’s commercial clients and private wealth management) and a good presence in Western Canada. NA is also doing very well in Cambodia (Aba Bank) and through its door into the U.S. (Credigy).

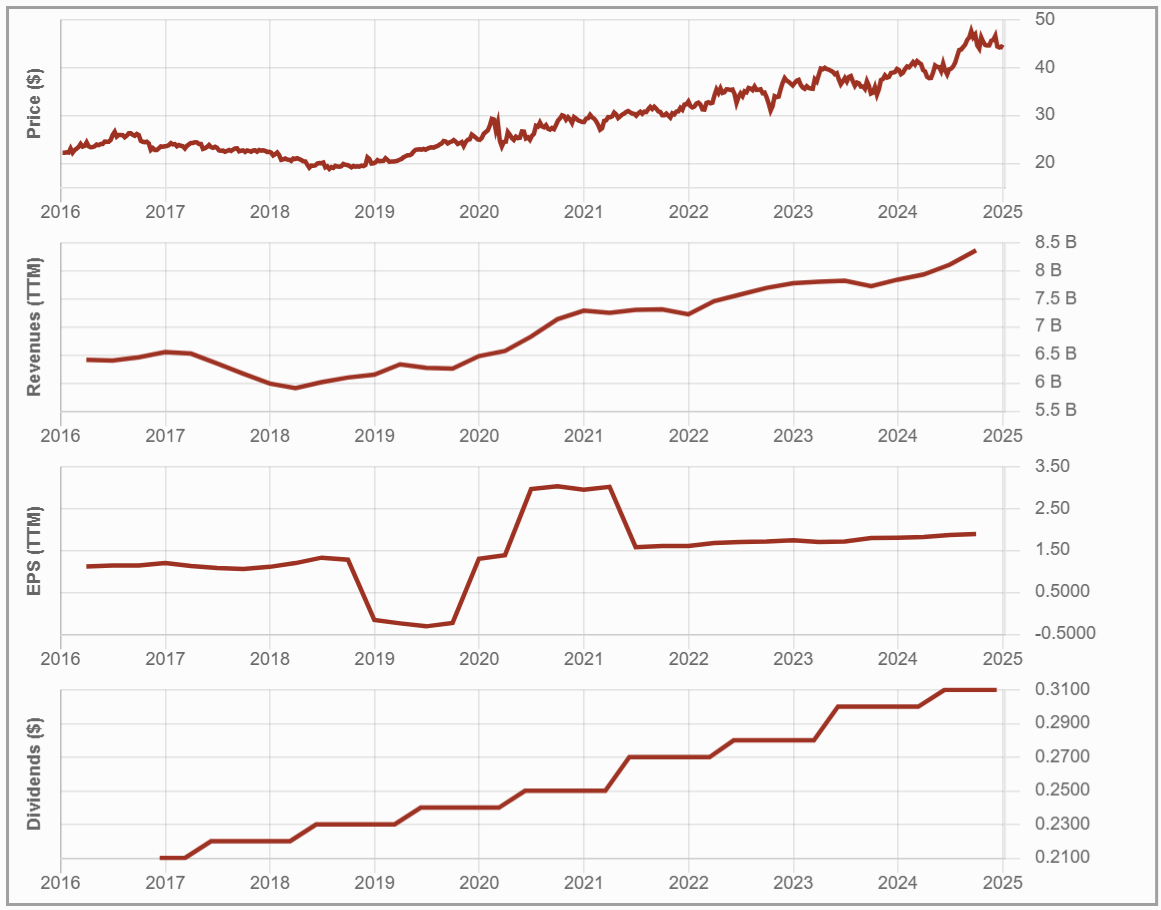

Hydro One (H.TO)

Business model

Hydro One is an electricity transmission and distribution provider in Ontario. The company’s segments include transmission, distribution, and other segments. The Transmission Segment comprises the transmission of high-voltage electricity across the province, interconnecting local distribution companies and specific large directly connected industrial customers throughout the Ontario electricity grid. The Distribution Segment comprises the delivery of electricity to end customers and certain other municipal electricity distributors.

What was the story?

From time to time, I hear that Hydro-Quebec should go public and unlock tons of value. However, I understand the government’s provincial view of keeping this fantastic asset for themselves. Do you know why? Because Hydro-Quebec pays a generous dividend to the government each year!

Well, Hydro One is in a similar situation, but you can get a piece of the cake as the Ontario Government decided to sell a part of its stake in this beauty. With 99% of its operations regulated and 98% of its electric lines in Ontario, an investment in Hydro One is a pure play on Ontario’s power development. This is the pure definition of a sleep-well-at-night investment. The company expects to invest $1.3B to $1.6B in CAPEX yearly until 2027, supporting their EPS growth guidance of 4-7% and dividend growth of about 5%. The province enjoys a substantial and diversified economy, and Hydro One will continue to grow by walking in the province’s path.

Don’t go just yet. Get more fantastic dividend stock ideas!

There are 6 more ideas of my top 27 for 2025 ready to be delivered to your emails!

The booklet includes dividend stocks selected with high standards in three sectors: Communication Services, Consumer Staples, and Industrials.

Each sector has been reviewed, and stocks were cherry-picked according to what’s coming. Get your copy now!

DGB –

I am going to dive into Fortis a bit more, love the Utility business model and do hold Dominion, as well. Great picks and as you said – you can hardly go wrong with a Canadian bank!

-Lanny

FTS is the ultimate money printing machine in Canada, you can’t go wrong 🙂

Cheers,